Choosing the best CD for your institution to invest in can be difficult. There are thousands of banks and credit unions across the country that offer various term and interest options. By reading this, we’ll help you determine if our certificates of deposit are your best fit. Our goal is to help you make the most rewarding investment decision possible.

Why buy directly online from Continental instead of a broker or wealth manager?

Flexibility and affordability. Our product offerings are flexible if you want to include additional features like unrestricted early withdrawals, or options to bump up your APY if rates rise. And we don’t charge you for the feature flexibility we offer. Brokers and asset managers charge either a commission, fee, or spread. When you buy directly from us, you typically enjoy a higher rate, and don’t get charged any commission, fee, or spread. Plus, you’re supporting the local, small-business economy. Continental Bank is an FDIC-insured commercial bank that specializes in providing equipment financing to small and medium-sized businesses nationwide.

What’s unique about Continental’s CDs?

- FDIC Coverage – Through CDARS we can provide FDIC insurance far above the standard $250,000.

- Lenient Early Withdrawal Penalties – Compare ours to our competitors—if you find the same CD term and structure with a better Early Withdrawal Penalty, we’ll match it!

- We’re Flexible – If you want a specific, customized CD term or structure—call us—we’ll provide a quote based on your specific needs.

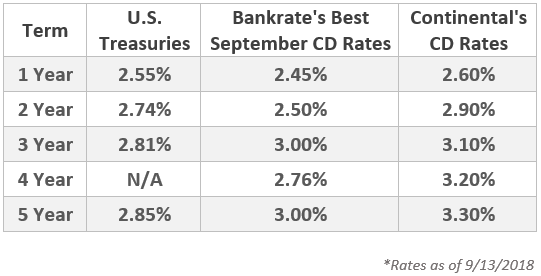

- High Rates – Bankrate disclosed their “Best CD Rates in September 2018” for each term on their website, and we’re pleased that our rates (for all like terms) are on average 10.3% higher!

How do Continental’s CD compare to Treasuries and Corporate Bonds?

In short, the longer the term, the more competitive Continental’s CDs are. On Wednesday, September 13th the yield on the 10-year Treasury fell to 2.96%—down from a recent high of 3.12% on May 17th. Over the same time, however, our CD rates have risen and now yield up to .45% more than like-term Treasuries, while still maintaining FDIC insurance. The longer the term, the greater our yield spread is over Treasuries, with our 5-year CD offering 45 basis points over the 5-year Treasury note.

But in addition to a better rate—and without having to bear any more risk—Continental’s CDs offer early withdrawals and flexible interest-payment options. On the other hand, one main advantage Treasuries have over certificates of deposit is their state tax exemption status, (most states are 5%). In all, we view Treasuries as a competitive alternative to Continental’s CDs if the term is less than 1 year. For more on this, check out DepositAccounts’ blog.

When comparing certificates of deposit to investment grade corporate floating-rate bonds (floaters), the two critical considerations to make are your near-term interest rate outlook and investment horizon. These two factors will largely determine whether a CD or a floater is better for you. The advantage floaters have over CDs when rates rise over the term of your investment are two-fold:

- Income payments rise as short-term interest rates rise

- Prices remain relatively stable, even if interest rates rise

The opposite is true when rates decline. Given Wall Street’s expectation that the Fed will raise rates two more times this year and likely into 2019, a floater would likely yield more (depending on the spread over LIBOR) if your investment horizon is less than two years. However, if you have the same rate outlook but are looking to invest for more than two years, it’s possible—even likely—that rates could fall below where they are now, giving a fixed-rate CD the edge. One disadvantage corporate floaters inherently have is their lack of FDIC insurance.

Don’t want to compromise by giving something up to get something else? In other words, don’t want to miss out on rising rates by being forced to take the risk that rates fall below their current levels before maturity? Buy a “Bump-up CD” that allows you to lock in a great rate now and have the opportunity to increase it (without extending the maturity) if rates rise.